Insurance is a vital financial tool that provides protection and peace of mind by mitigating the financial risks associated with unexpected events. There are various types of insurance available, each designed to address specific needs and risks. In this guide, we’ll explain the different types of insurance, their purposes, and how they work.

Table of Contents

- Introduction to Insurance Types

- Defining Insurance

- Why Insurance Matters

- Types of Personal Insurance

- Health Insurance

- Life Insurance

- Disability Insurance

- Auto Insurance

- Homeowners or Renters Insurance

- Types of Business Insurance

- General Liability Insurance

- Property Insurance

- Workers’ Compensation Insurance

- Professional Liability Insurance

- Business Interruption Insurance

- Specialized Insurance

- Travel Insurance

- Pet Insurance

- Flood Insurance

- Cyber Insurance

- Choosing the Right Insurance

- Assessing Your Needs

- Comparing Policies

- Working with an Agent

- Conclusion

1. Introduction to Insurance Types

Defining Insurance

Insurance is a contractual arrangement between an individual, business, or entity (the policyholder) and an insurance company (the insurer). In exchange for regular premium payments, the insurer agrees to provide financial protection in case of specific predefined events or losses.

Why Insurance Matters

Insurance serves as a safety net, reducing the financial impact of unexpected events. It offers peace of mind by covering expenses that could otherwise be financially devastating. It also promotes economic stability by spreading risk across a large pool of policyholders.

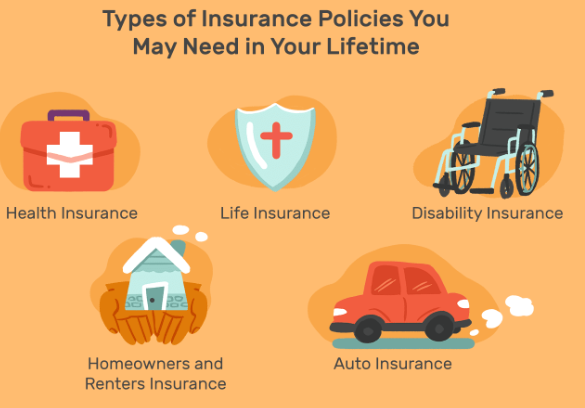

2. Types of Personal Insurance

Health Insurance

Health insurance covers medical expenses, including doctor visits, hospital stays, prescription drugs, and preventive care. It helps individuals manage healthcare costs and access necessary medical services.

Life Insurance

Life insurance provides a payout to beneficiaries (typically family members) upon the policyholder’s death. It offers financial protection and can be used to replace income, pay off debts, or cover funeral expenses.

Disability Insurance

Disability insurance pays a portion of the policyholder’s income if they become disabled and cannot work. It ensures financial stability during periods of disability.

Auto Insurance

Auto insurance covers damages and injuries resulting from accidents involving vehicles. It often includes liability coverage, collision coverage, and comprehensive coverage.

Homeowners or Renters Insurance

Homeowners insurance protects the physical structure of a home and its contents from damage or theft. Renters insurance covers personal belongings for individuals renting homes or apartments.

3. Types of Business Insurance

General Liability Insurance

General liability insurance protects businesses from claims of bodily injury or property damage caused by their operations. It covers legal expenses and settlements.

Property Insurance

Property insurance covers physical assets such as buildings, equipment, and inventory against damage or loss due to events like fires, storms, or theft.

Workers’ Compensation Insurance

Workers’ compensation insurance compensates employees for work-related injuries or illnesses, covering medical expenses and lost wages. It’s often required for businesses with employees.

Professional Liability Insurance

Professional liability insurance (also known as errors and omissions or E&O insurance) protects professionals from claims of negligence or errors in their professional services. It’s essential for doctors, lawyers, consultants, and other service providers.

Business Interruption Insurance

Business interruption insurance covers lost income and operating expenses if a business is unable to operate due to a covered event, such as a fire or natural disaster.

4. Specialized Insurance

Travel Insurance

Travel insurance provides coverage for trip cancellations, medical emergencies, lost baggage, and other travel-related issues. It’s essential for travelers, especially when going abroad.

Pet Insurance

Pet insurance covers veterinary expenses for pets. It helps pet owners manage healthcare costs and ensures their furry companions receive necessary medical care.

Flood Insurance

Flood insurance covers damages caused by flooding, which is typically not included in standard homeowners or renters insurance policies.

Cyber Insurance

Cyber insurance protects businesses from the financial impact of data breaches and cyberattacks. It covers expenses related to data recovery, legal fees, and notifying affected parties.

5. Choosing the Right Insurance

Assessing Your Needs

To choose the right insurance, assess your specific needs and risks. Consider your lifestyle, financial situation, and any legal requirements.

Comparing Policies

Compare policies from multiple insurers to find the best coverage and rates. Look at coverage limits, deductibles, and exclusions.

Working with an Agent

Consult with an experienced insurance agent who can provide expert guidance and help you tailor policies to your unique needs.

6. Conclusion

Insurance is a crucial financial tool that provides protection and peace of mind in various aspects of life, from healthcare to business operations. By understanding the different types of insurance and selecting the right coverage for your specific needs, you can effectively manage risks and ensure financial stability in the face of unexpected events.